All Categories

Featured

Table of Contents

The are entire life insurance and universal life insurance. The cash money worth is not included to the fatality advantage.

After one decade, the cash value has actually grown to roughly $150,000. He obtains a tax-free lending of $50,000 to start a company with his sibling. The policy finance rates of interest is 6%. He pays back the loan over the next 5 years. Going this route, the rate of interest he pays returns right into his plan's cash worth rather than an economic institution.

Become My Own Bank

Nash was a finance professional and follower of the Austrian college of economics, which advocates that the worth of goods aren't explicitly the outcome of standard financial frameworks like supply and need. Rather, people value money and products differently based on their financial standing and demands.

Among the pitfalls of conventional financial, according to Nash, was high-interest prices on financings. A lot of people, himself consisted of, entered economic trouble because of dependence on banking organizations. Long as financial institutions set the interest rates and car loan terms, people didn't have control over their very own riches. Becoming your very own banker, Nash figured out, would certainly put you in control over your monetary future.

Infinite Banking requires you to have your economic future. For ambitious individuals, it can be the ideal financial tool ever before. Here are the benefits of Infinite Banking: Probably the single most helpful element of Infinite Banking is that it improves your cash money flow.

Dividend-paying entire life insurance policy is extremely low threat and provides you, the insurance policy holder, a lot of control. The control that Infinite Banking uses can best be grouped right into two categories: tax obligation benefits and possession protections - public bank visa infinite. One of the reasons whole life insurance policy is excellent for Infinite Financial is exactly how it's strained.

Whole Life Banking

When you use whole life insurance policy for Infinite Banking, you become part of an exclusive agreement between you and your insurer. This privacy uses particular asset securities not located in various other monetary cars. These protections might vary from state to state, they can include defense from asset searches and seizures, protection from reasonings and defense from lenders.

Entire life insurance policy policies are non-correlated possessions. This is why they function so well as the economic foundation of Infinite Banking. No matter what takes place on the market (stock, realty, or otherwise), your insurance plan retains its well worth. Too numerous people are missing this crucial volatility barrier that helps safeguard and expand riches, rather breaking their money right into 2 containers: bank accounts and financial investments.

Entire life insurance coverage is that third bucket. Not only is the rate of return on your entire life insurance plan guaranteed, your fatality advantage and premiums are also ensured.

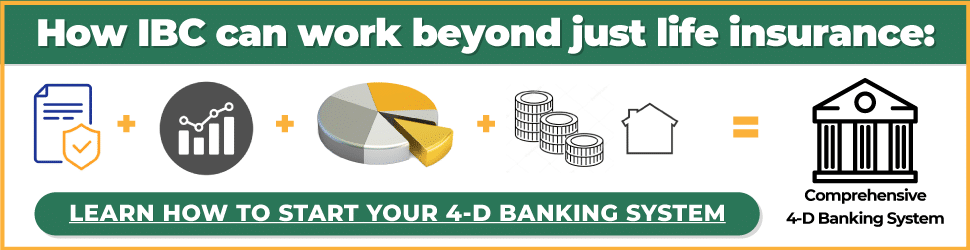

This framework lines up perfectly with the concepts of the Continuous Wealth Approach. Infinite Banking interest those looking for better monetary control. Here are its primary benefits: Liquidity and availability: Policy car loans offer instant access to funds without the restrictions of conventional financial institution lendings. Tax obligation performance: The cash value expands tax-deferred, and policy fundings are tax-free, making it a tax-efficient device for developing wealth.

Infinity Banking

Asset security: In several states, the money worth of life insurance coverage is secured from lenders, including an added layer of financial safety and security. While Infinite Financial has its benefits, it isn't a one-size-fits-all option, and it features considerable disadvantages. Here's why it might not be the most effective strategy: Infinite Banking usually requires complex policy structuring, which can puzzle policyholders.

Envision never having to fret about bank fundings or high rate of interest once more. What happens if you could borrow money on your terms and build riches all at once? That's the power of infinite financial life insurance policy. By leveraging the money value of entire life insurance coverage IUL plans, you can grow your wealth and obtain money without depending on conventional financial institutions.

There's no collection finance term, and you have the flexibility to choose the payment routine, which can be as leisurely as repaying the lending at the time of fatality. This versatility prolongs to the maintenance of the financings, where you can go with interest-only settlements, keeping the loan balance flat and manageable.

Holding cash in an IUL dealt with account being attributed interest can commonly be better than holding the cash on down payment at a bank.: You've always dreamed of opening your very own bakery. You can obtain from your IUL plan to cover the first expenses of renting out a space, acquiring equipment, and hiring team.

Ray Poteet Infinite Banking

Individual loans can be gotten from typical banks and credit history unions. Obtaining cash on a credit rating card is usually really expensive with annual percent rates of rate of interest (APR) frequently reaching 20% to 30% or more a year.

The tax therapy of policy fundings can differ significantly depending on your nation of home and the certain terms of your IUL plan. In some areas, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are typically tax-free, offering a considerable advantage. Nonetheless, in other jurisdictions, there may be tax ramifications to consider, such as possible taxes on the lending.

Term life insurance coverage just provides a fatality advantage, without any money worth accumulation. This suggests there's no money value to obtain against.

Nevertheless, for financing officers, the substantial policies imposed by the CFPB can be seen as difficult and limiting. Initially, funding policemans frequently argue that the CFPB's guidelines produce unneeded red tape, leading to more documents and slower finance handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while focused on safeguarding customers, can cause delays in closing deals and increased functional costs.

{kind=link}

Table of Contents

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example

More

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example