All Categories

Featured

Table of Contents

For many people, the largest problem with the unlimited financial concept is that initial hit to early liquidity caused by the prices. Although this disadvantage of boundless financial can be minimized substantially with appropriate plan style, the first years will constantly be the most awful years with any type of Whole Life plan.

That claimed, there are particular limitless financial life insurance coverage policies designed mainly for high early cash worth (HECV) of over 90% in the initial year. The long-term performance will certainly frequently substantially delay the best-performing Infinite Financial life insurance plans. Having access to that extra 4 numbers in the initial couple of years might come at the expense of 6-figures down the road.

You actually obtain some considerable lasting advantages that assist you recover these very early expenses and after that some. We find that this impeded early liquidity problem with infinite banking is more mental than anything else as soon as thoroughly discovered. In truth, if they definitely needed every cent of the money missing from their unlimited banking life insurance coverage plan in the initial few years.

Tag: boundless financial principle In this episode, I speak regarding financial resources with Mary Jo Irmen that teaches the Infinite Banking Idea. With the surge of TikTok as an information-sharing system, monetary advice and strategies have actually discovered a novel way of spreading. One such strategy that has been making the rounds is the boundless financial concept, or IBC for short, garnering recommendations from celebs like rap artist Waka Flocka Fire.

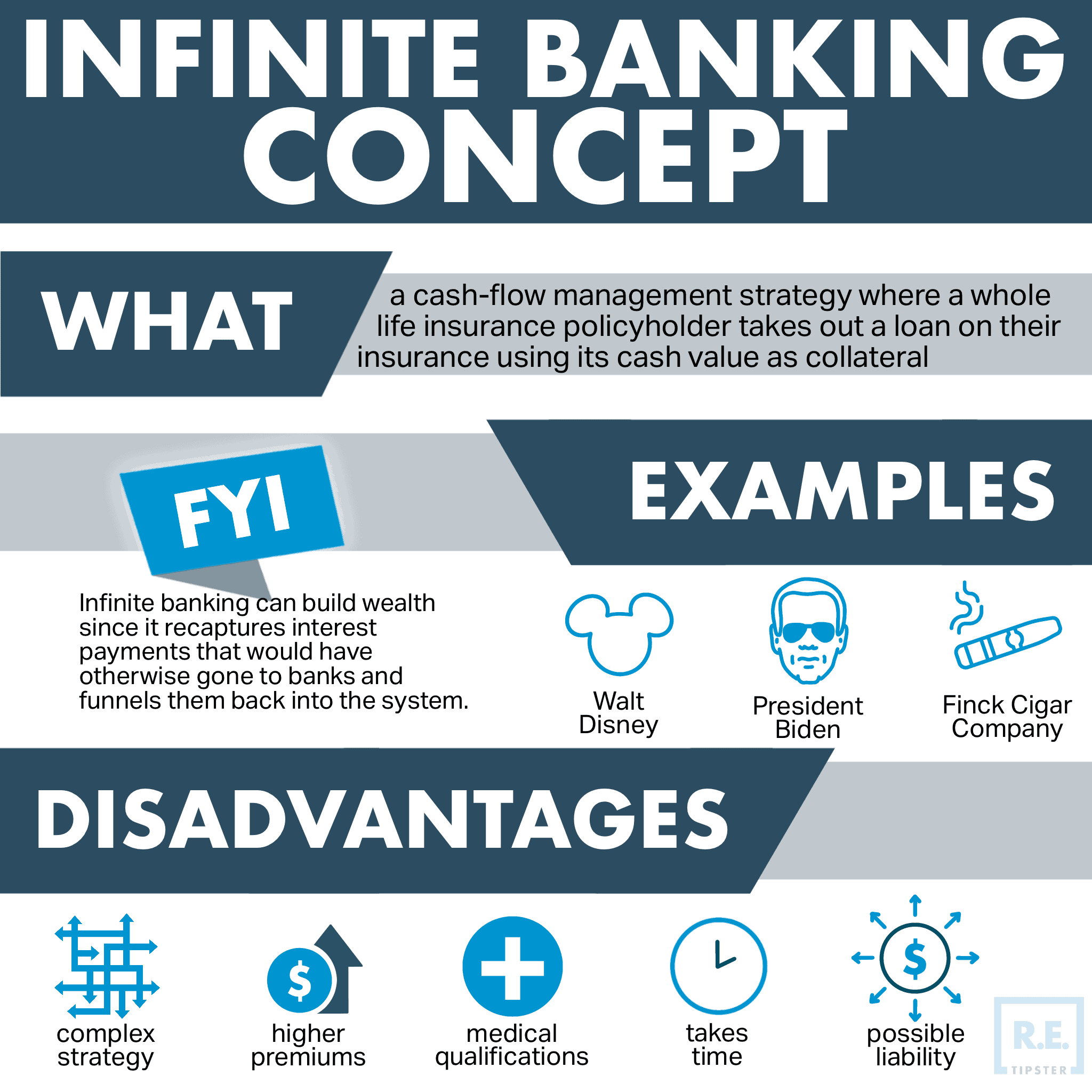

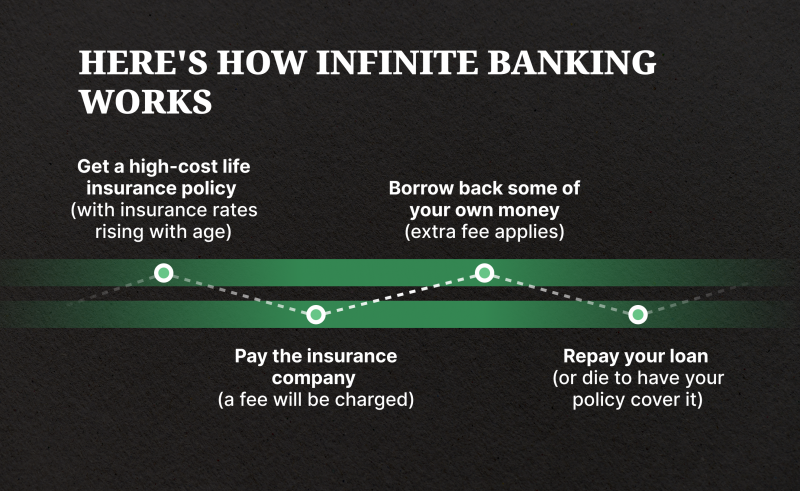

Within these policies, the cash value grows based on a rate established by the insurer. When a considerable cash worth gathers, insurance policy holders can obtain a cash worth financing. These car loans differ from standard ones, with life insurance policy working as collateral, meaning one can lose their coverage if borrowing excessively without ample cash money value to support the insurance costs.

And while the appeal of these plans appears, there are natural constraints and threats, requiring persistent cash money value surveillance. The approach's legitimacy isn't black and white. For high-net-worth people or company proprietors, specifically those using techniques like company-owned life insurance coverage (COLI), the advantages of tax breaks and compound development could be appealing.

What Is A Cash Flow Banking System

The appeal of unlimited financial does not negate its challenges: Cost: The fundamental demand, a long-term life insurance policy policy, is more expensive than its term equivalents. Qualification: Not everybody certifies for entire life insurance because of extensive underwriting procedures that can omit those with specific health and wellness or way of living conditions. Complexity and danger: The detailed nature of IBC, coupled with its dangers, may discourage numerous, specifically when less complex and less risky alternatives are readily available.

Assigning around 10% of your regular monthly revenue to the policy is just not viable for most people. Part of what you review below is just a reiteration of what has actually already been stated above.

Prior to you obtain yourself right into a situation you're not prepared for, recognize the complying with initially: Although the idea is typically offered as such, you're not in fact taking a loan from yourself. If that were the instance, you wouldn't have to repay it. Rather, you're borrowing from the insurer and have to repay it with interest.

Some social networks articles advise utilizing cash value from entire life insurance to pay down charge card financial obligation. The idea is that when you pay back the lending with passion, the amount will be returned to your investments. Sadly, that's not just how it functions. When you pay back the financing, a section of that interest mosts likely to the insurance coverage firm.

For the first several years, you'll be paying off the compensation. This makes it extremely challenging for your policy to accumulate value throughout this time. Unless you can afford to pay a few to several hundred bucks for the following decade or even more, IBC will not function for you.

Visa Infinite Rewards Royal Bank

If you require life insurance, below are some useful tips to take into consideration: Think about term life insurance. Make certain to go shopping around for the ideal rate.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Style Call "Montserrat".

Whole Life Insurance Banking

As a certified public accountant specializing in property investing, I've cleaned shoulders with the "Infinite Banking Idea" (IBC) more times than I can count. I've also talked to professionals on the topic. The major draw, other than the obvious life insurance benefits, was constantly the idea of constructing up money value within a long-term life insurance policy and loaning versus it.

Certain, that makes good sense. Yet truthfully, I always assumed that cash would be better invested directly on investments rather than funneling it via a life insurance plan Till I uncovered how IBC might be integrated with an Irrevocable Life Insurance Trust (ILIT) to create generational riches. Let's begin with the essentials.

Royal Bank Infinite Avion Points

When you obtain versus your policy's cash worth, there's no collection payment routine, offering you the freedom to manage the financing on your terms. On the other hand, the cash money worth proceeds to expand based on the policy's assurances and rewards. This setup permits you to access liquidity without interrupting the long-lasting growth of your policy, gave that the finance and interest are taken care of wisely.

As grandchildren are born and expand up, the ILIT can buy life insurance policy plans on their lives. Household members can take lendings from the ILIT, making use of the cash worth of the plans to fund investments, begin organizations, or cover significant expenditures.

A critical aspect of handling this Household Bank is using the HEMS criterion, which means "Health and wellness, Education, Upkeep, or Support." This guideline is commonly consisted of in trust fund contracts to direct the trustee on exactly how they can distribute funds to recipients. By sticking to the HEMS standard, the depend on makes sure that circulations are made for necessary requirements and long-term support, protecting the trust's properties while still attending to relative.

Boosted Flexibility: Unlike stiff bank fundings, you regulate the repayment terms when borrowing from your very own policy. This enables you to structure payments in a means that straightens with your service capital. infinite banking insurance companies. Better Capital: By financing overhead via policy loans, you can possibly free up cash money that would certainly or else be locked up in conventional lending repayments or equipment leases

He has the exact same tools, yet has actually additionally built added cash money value in his plan and received tax obligation benefits. Plus, he currently has $50,000 available in his policy to use for future possibilities or expenses., it's vital to view it as more than simply life insurance policy.

Rbc Private Banking Visa Infinite Card

It has to do with creating a flexible financing system that gives you control and offers several advantages. When utilized strategically, it can match other investments and business techniques. If you're interested by the capacity of the Infinite Banking Concept for your business, here are some steps to think about: Inform Yourself: Dive much deeper into the principle with trusted books, seminars, or consultations with experienced professionals.

{kind=link}

Table of Contents

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example

More

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example