All Categories

Featured

Table of Contents

For many people, the biggest issue with the boundless financial concept is that first hit to early liquidity brought on by the expenses. Although this disadvantage of unlimited financial can be reduced substantially with proper policy layout, the initial years will certainly always be the worst years with any type of Whole Life plan.

That claimed, there are certain limitless banking life insurance policy plans developed mainly for high very early cash money worth (HECV) of over 90% in the initial year. The long-lasting performance will usually significantly lag the best-performing Infinite Financial life insurance coverage plans. Having accessibility to that added four figures in the initial couple of years may come at the expense of 6-figures in the future.

You actually get some substantial lasting benefits that help you recoup these early prices and afterwards some. We locate that this hindered early liquidity problem with unlimited financial is much more mental than anything else as soon as extensively checked out. If they absolutely needed every cent of the money missing from their infinite financial life insurance coverage policy in the initial few years.

Tag: limitless banking idea In this episode, I chat regarding financial resources with Mary Jo Irmen that educates the Infinite Banking Principle. With the surge of TikTok as an information-sharing system, financial recommendations and strategies have actually discovered a novel means of spreading. One such technique that has been making the rounds is the infinite banking idea, or IBC for short, garnering recommendations from celebrities like rapper Waka Flocka Flame.

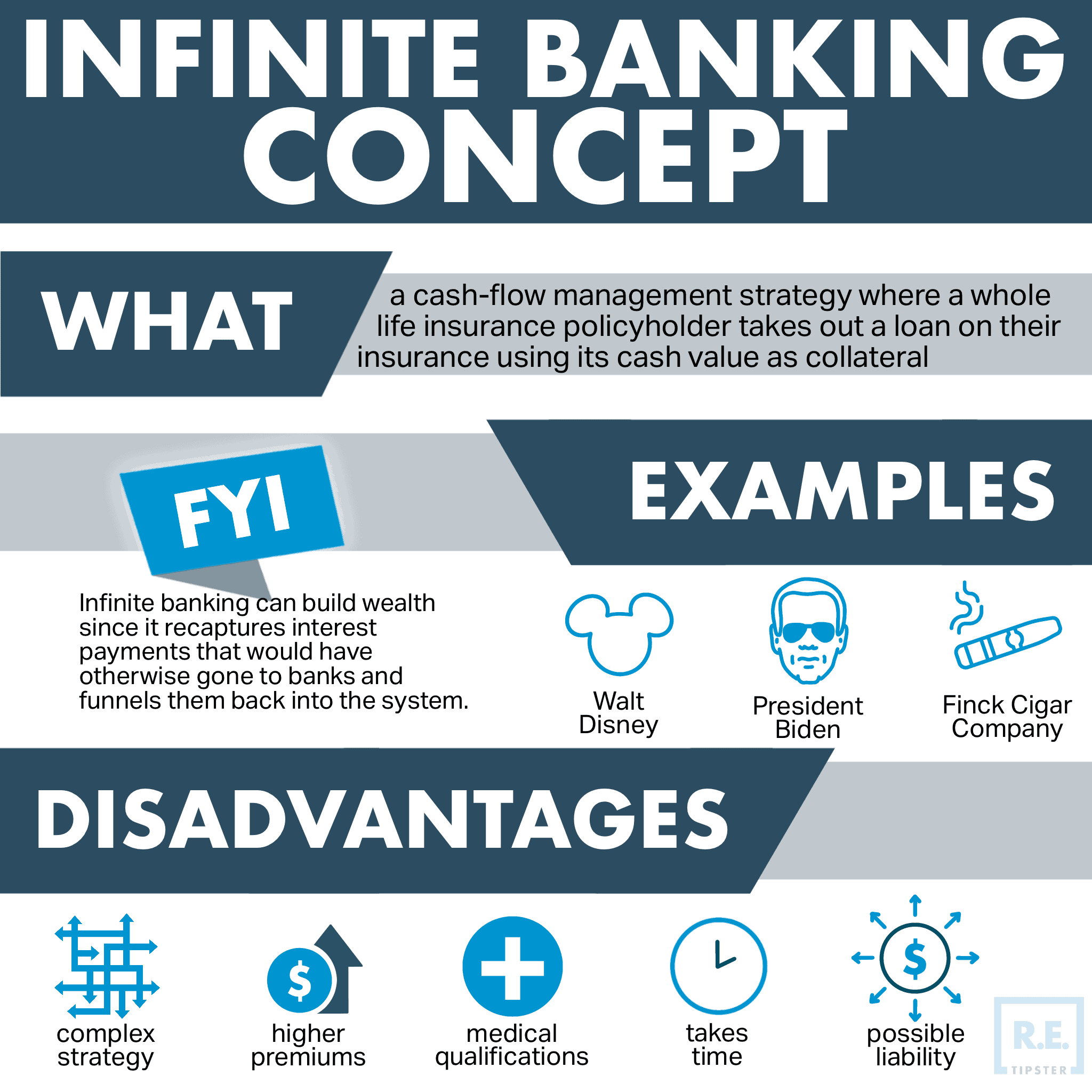

Within these plans, the cash value grows based on a rate established by the insurance provider. Once a significant cash money value builds up, insurance policy holders can acquire a money value finance. These loans differ from conventional ones, with life insurance policy functioning as security, implying one could lose their protection if borrowing excessively without adequate cash value to support the insurance coverage costs.

And while the allure of these policies appears, there are natural constraints and threats, requiring thorough money value monitoring. The strategy's authenticity isn't black and white. For high-net-worth people or organization owners, specifically those using strategies like company-owned life insurance (COLI), the advantages of tax breaks and substance development might be appealing.

Infinite Banking Concept Scam

The allure of limitless financial does not negate its challenges: Expense: The fundamental need, a long-term life insurance coverage plan, is more expensive than its term counterparts. Qualification: Not everyone gets entire life insurance policy because of strenuous underwriting procedures that can omit those with specific health or way of life conditions. Complexity and risk: The intricate nature of IBC, coupled with its threats, may prevent numerous, specifically when less complex and much less high-risk choices are available.

Alloting around 10% of your regular monthly income to the policy is simply not practical for many individuals. Component of what you read below is just a reiteration of what has actually currently been said above.

Prior to you get yourself right into a circumstance you're not prepared for, recognize the adhering to first: Although the principle is frequently sold as such, you're not actually taking a financing from yourself. If that held true, you wouldn't have to settle it. Instead, you're borrowing from the insurance policy business and have to settle it with rate of interest.

Some social media articles recommend using cash value from whole life insurance to pay down credit report card financial debt. When you pay back the finance, a section of that rate of interest goes to the insurance coverage firm.

For the very first a number of years, you'll be paying off the payment. This makes it exceptionally challenging for your policy to build up value throughout this time. Unless you can pay for to pay a couple of to numerous hundred dollars for the following decade or more, IBC will not function for you.

Bioshock Infinite Bank Of The Prophet Elevator

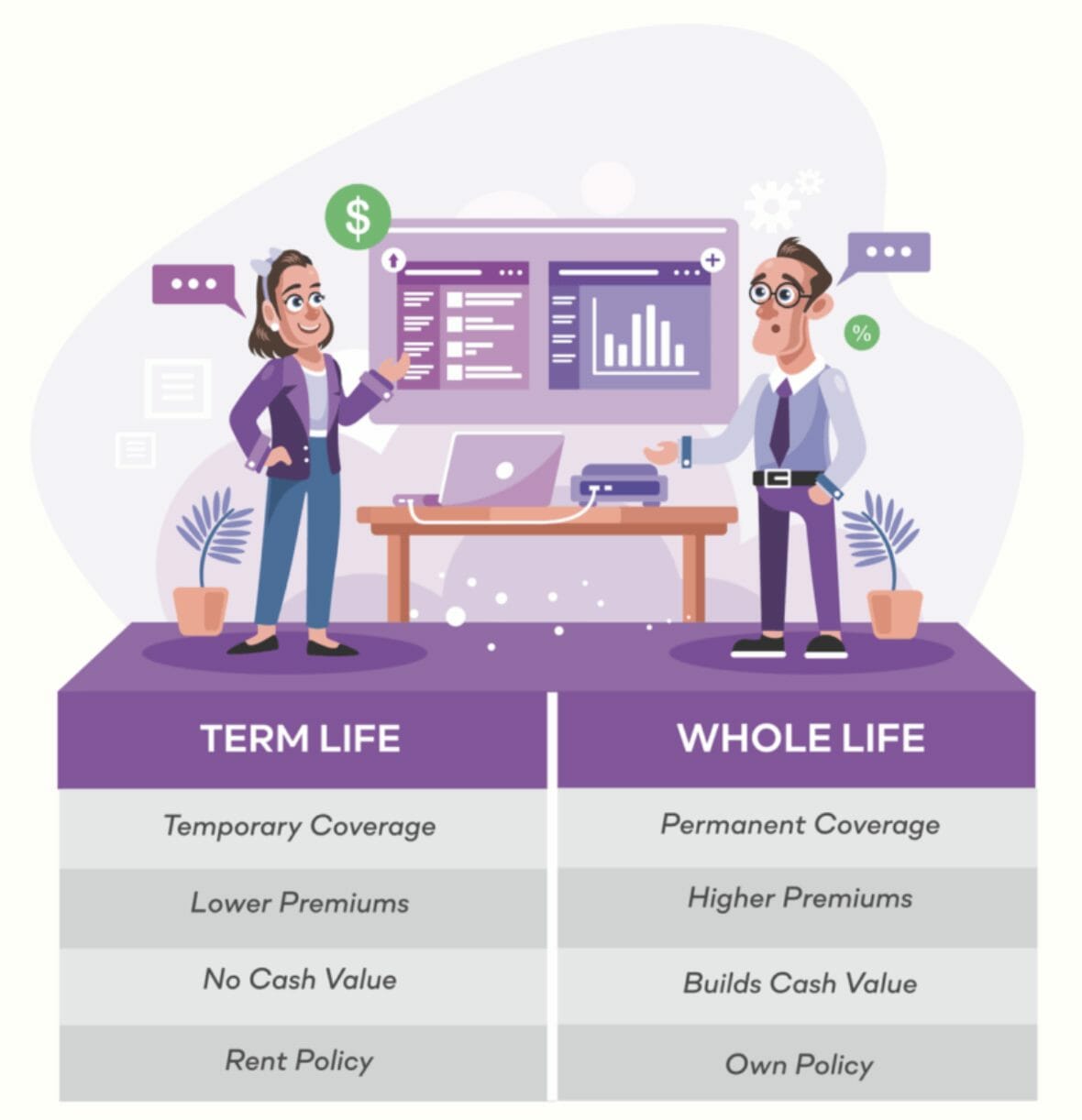

If you call for life insurance coverage, right here are some useful tips to consider: Think about term life insurance policy. Make certain to go shopping around for the ideal rate.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Typeface Name "Montserrat". This Typeface Software is certified under the SIL Open Up Typeface Certificate, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Typeface Call "Montserrat". This Typeface Software is certified under the SIL Open Up Typeface Permit, Version 1.1.Avoid to main content

Whole Life Concept

As a certified public accountant concentrating on realty investing, I have actually cleaned shoulders with the "Infinite Financial Concept" (IBC) more times than I can count. I have actually even talked to professionals on the subject. The major draw, aside from the apparent life insurance policy advantages, was constantly the idea of constructing up cash money worth within a long-term life insurance plan and borrowing versus it.

Certain, that makes sense. Yet truthfully, I constantly thought that cash would be much better spent straight on financial investments rather than funneling it with a life insurance plan Until I uncovered just how IBC might be incorporated with an Irrevocable Life Insurance Coverage Count On (ILIT) to produce generational wealth. Allow's begin with the essentials.

How To Start Infinite Banking

When you obtain versus your plan's cash money worth, there's no set settlement routine, providing you the flexibility to take care of the funding on your terms. The cash money worth continues to expand based on the plan's warranties and dividends. This arrangement permits you to accessibility liquidity without interfering with the long-lasting development of your policy, supplied that the finance and rate of interest are handled sensibly.

The process continues with future generations. As grandchildren are born and expand up, the ILIT can purchase life insurance plans on their lives. The depend on then builds up several policies, each with growing money values and survivor benefit. With these policies in location, the ILIT effectively becomes a "Household Bank." Member of the family can take car loans from the ILIT, utilizing the cash money worth of the plans to money investments, start companies, or cover major costs.

A critical element of managing this Household Bank is making use of the HEMS requirement, which stands for "Wellness, Education, Upkeep, or Assistance." This guideline is usually included in count on agreements to direct the trustee on just how they can distribute funds to beneficiaries. By sticking to the HEMS requirement, the trust fund guarantees that distributions are made for vital requirements and long-lasting assistance, protecting the trust's assets while still supplying for member of the family.

Raised Flexibility: Unlike rigid small business loan, you regulate the settlement terms when borrowing from your very own plan. This allows you to structure payments in a means that straightens with your business capital. infinite banking policy. Improved Money Flow: By financing service costs with plan lendings, you can possibly maximize cash money that would certainly or else be bound in typical loan repayments or tools leases

He has the exact same devices, however has also developed added cash money worth in his plan and received tax advantages. Plus, he now has $50,000 available in his policy to make use of for future opportunities or expenditures. Regardless of its possible benefits, some people continue to be doubtful of the Infinite Financial Idea. Allow's resolve a couple of common worries: "Isn't this simply expensive life insurance policy?" While it's true that the premiums for an appropriately structured entire life plan may be more than term insurance policy, it is essential to watch it as greater than just life insurance policy.

Dave Ramsey Infinite Banking Concept

It has to do with producing an adaptable funding system that gives you control and offers multiple benefits. When made use of strategically, it can match various other investments and company approaches. If you're captivated by the capacity of the Infinite Banking Idea for your company, here are some steps to think about: Enlighten Yourself: Dive much deeper right into the idea through respectable publications, seminars, or examinations with well-informed specialists.

{kind=link}

Table of Contents

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example

More

Latest Posts

Infinite Banking Agents

Becoming Your Own Bank

Infinite Banking Example